The global seaborne coal market has grown yet again, over the course of the first half of 2022, following the significant rise of 2021. In its latest weekly report, shipbroker Banchero Costa said that “following a disastrous 2020, with the world hit by lockdowns and recession pretty much everywhere, global seaborne coal trade managed to rebound to some extent in 2021. In the full 12 months of 2021, global seaborne coal exports increased by +4.5% y-o-y to 1149 mln tonnes, from 1099 mln tonnes in 2020, according to vessels tracking data from Refinitiv. This however was still well below the levels we had in pre-Covid times, being -10.0% down from the 1276 mln tonnes shipped during 2019. In the first half of 2022, global coal trade was a bit of a mixed picture. In the January to June period of 2022, global coal loadings increased by +1.5% y-o-y to 572.7 mln t, from 564.1 mln t in the first half of 2021, but still well below the 637.9 mln t in 1H 2019. However, the worst was at start of the year, and the trend in recent months has been very positive. In 1Q 2022, global coal loadings were down -5.1% y-o-y to just 258.5 mln t. In 2Q 2022, coal loadings were a strong +7.7% y-o-y at 314.2 mln t. The month of June 2022 was actually a record 111.6 mln t, +12.3% y-o-y.

Source: banchero costa &c s.p.a

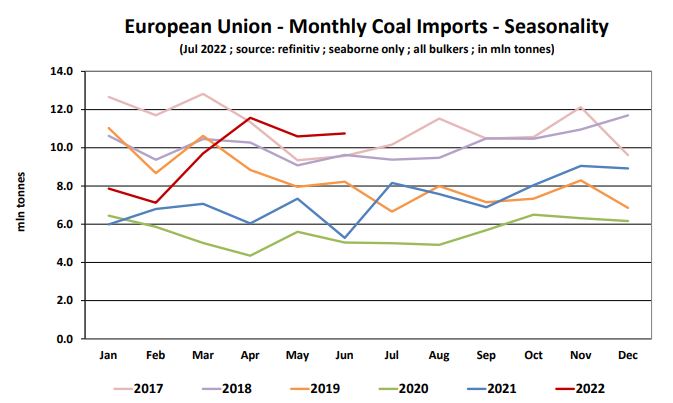

According to the shipbroker, “the European Union is now the fifth largest seaborne importer of coal in the world, after India, China, Japan and South Korea. In 1H 2022, the EU accounted for 10.4% of global seaborne coal shipments. The EU’s seaborne coal imports in the 12 months of 2021 increased by +30.3% y-o-y to 87.1 mln tonnes. This was mostly a rebound from a massive -32.9% y-o-y decline in 2020 caused by Covid lockdowns. Previous years also saw a negative trend, with European coal imports declining by -18.3% y-o-y in 2019 and by -7.6% y-o-y in 2018, as European countries progressively abandon coal as a source of energy and embrace natural gas and renewables. In the first 6 months of 2022, coal imports into the EU further increased by +49.6% y-o-y to 57.6 mln tonnes. Europe accelerated its coal imports as a direct reaction to the threat of a reduction in gas supply from Russia. This compensated for the sharp drop in demand from Mainland China”.

Banchero Costa added that “in 1H 2022, China’s seaborne coal imports declined by -26.0% y-o-y to 87.8 mln t, from 118.6 mln t in the same period of 2021. The main coal import terminals in the European Union (27) are: Rotterdam in the Netherlands (14.6 mln tonnes discharged in 1H 2022), Amsterdam Netherlands (6.8 mln tonnes), Hamburg Germany (3.0 mln tonnes), Gdansk Poland (3.0), Gijon Spain (2.8), Dunkirk France (1.9), Fos France (1.9), Ljmuiden Netherlands (1.6), Ghent Belgium (1.2), Vlissingen Netherlands (1.2), Plonce Croatia (1.2), Taranto Italy (1.1), Wilhelmshaven Germany (1.1), Koper Slovenia (1.0), Antwerp (1.0), Algeciras Spain (0.8). In terms of sources of the shipments, Europe was and still now remains heavily dependant on Russia. In the whole of 2021, as much as 44% of the EU’s seaborne coal imports were sourced from Russia. In 1H 2022, as a result of the war in Ukraine, this proportion has declined. Nevertheless, Russia was still the source of 31.5% of the EU’s coal imports this year, and remains as the top supplier of coal to Europe. In 1H 2022, coal imports to the EU from Russia increased by +0.2% y-o-y to 18.2 mln tonnes. Of this, 9.1 mln tonnes were imported in the first quarter of 2022 (-1.6% y-oy), and 9.0 mln tonnes were imported in the second quarter (+2.1% y-o-y)”.

Source: banchero costa &c s.p.a

“The second most important supplier to Europe is now the USA, accounting for 19.4% of Europe’s imports in 1H 2022. In 1H 2022, imports from the USA surged by +91.6% y-o-y to 11.2 mln t. The third largest supplier to Europe is Australia, accounting for 17.6% of the EU’s seaborne imports in 1H 2022. In 1H 2022, imports from Australia increased +27.3% y-o-y to 10.2 mln t. In fourth place was Colombia, with a 12.7% share of Europe’s coal imports. In 1H 2022, 7.3 mln tonnes were imported from Colombia to the EU, up +113.6% y-o-y. In fifth place was South Africa, with a 5.6% share of Europe’s coal imports. In 1H 2022, the EU imported 3.2 mln tonnes from South Africa, up +764.4% y-o-y from just 0.4 mln t in 1H 2021”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide